Invest Right, Invest Now With Upstox Trusted by 1 Crore+ Indians

-

4.4+

Avg. App rating

-

₹0

AMC -

₹20

Brokerage* -

Backed by the best

Backed by the best

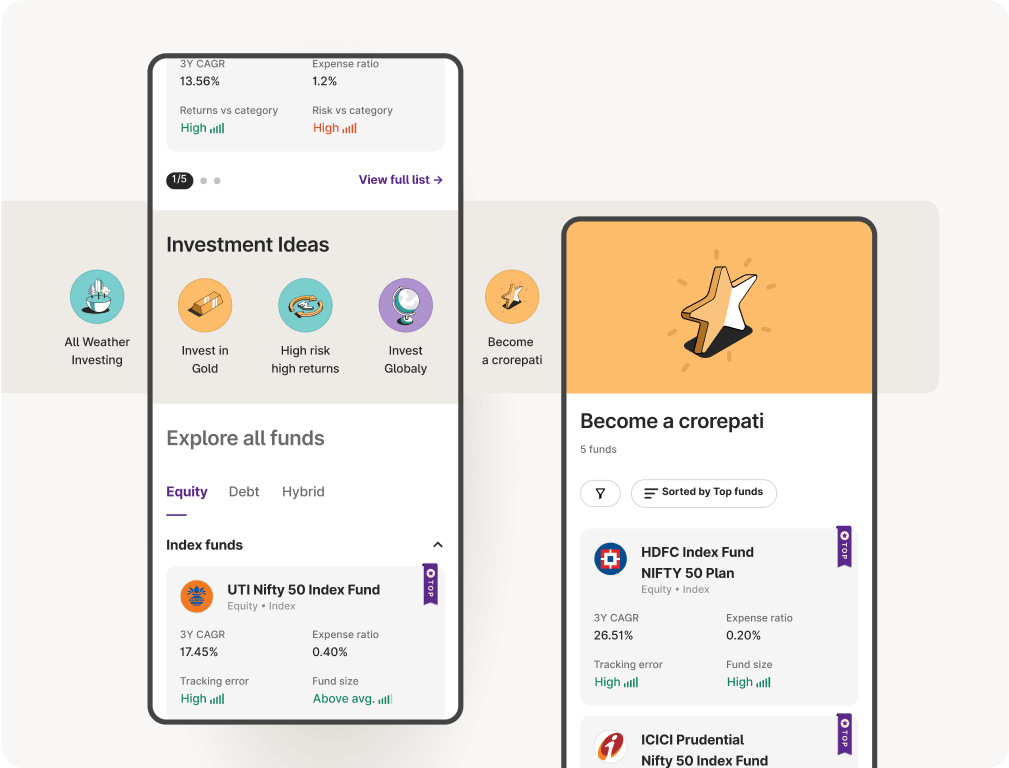

Upstox for Investors

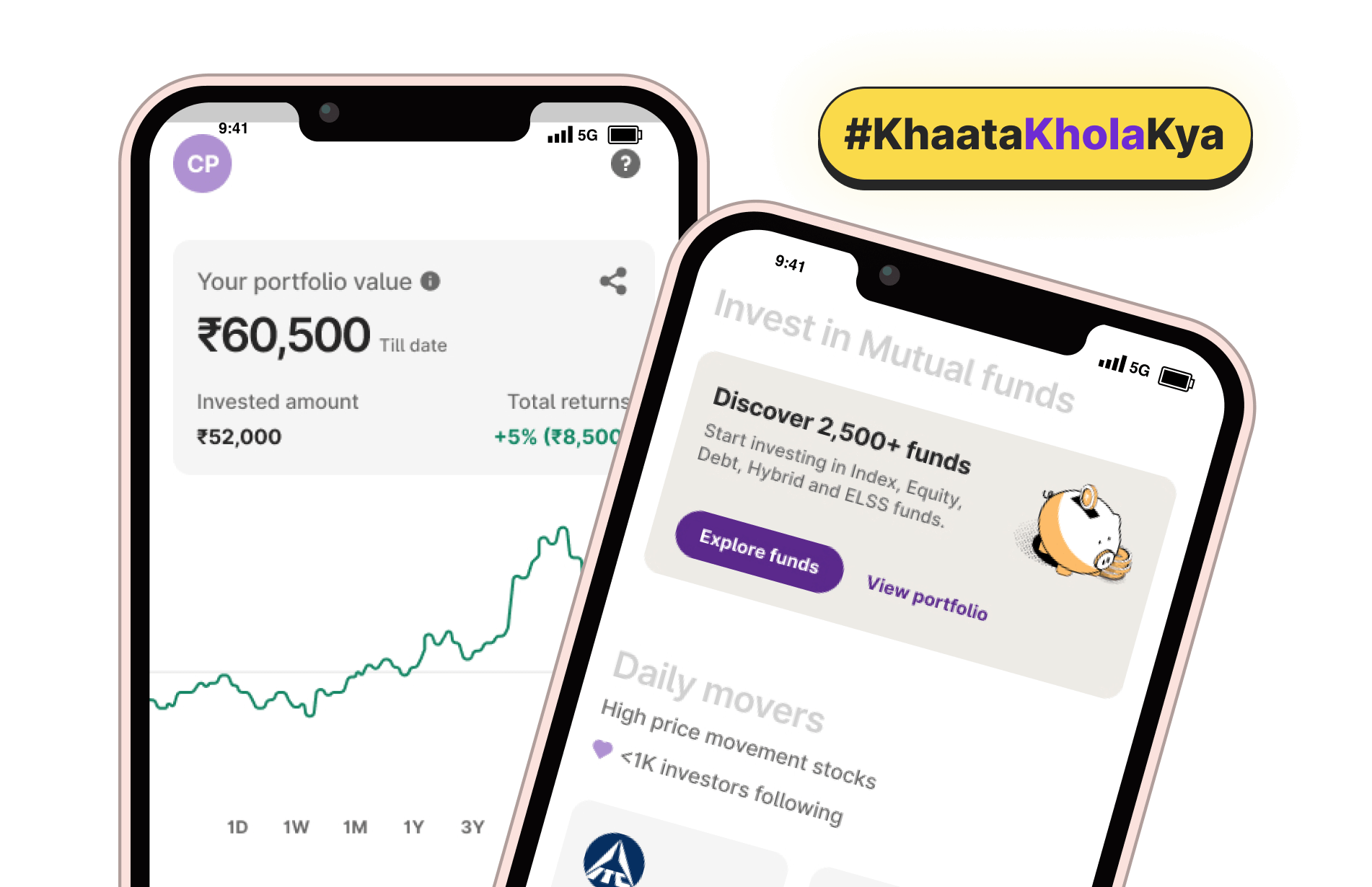

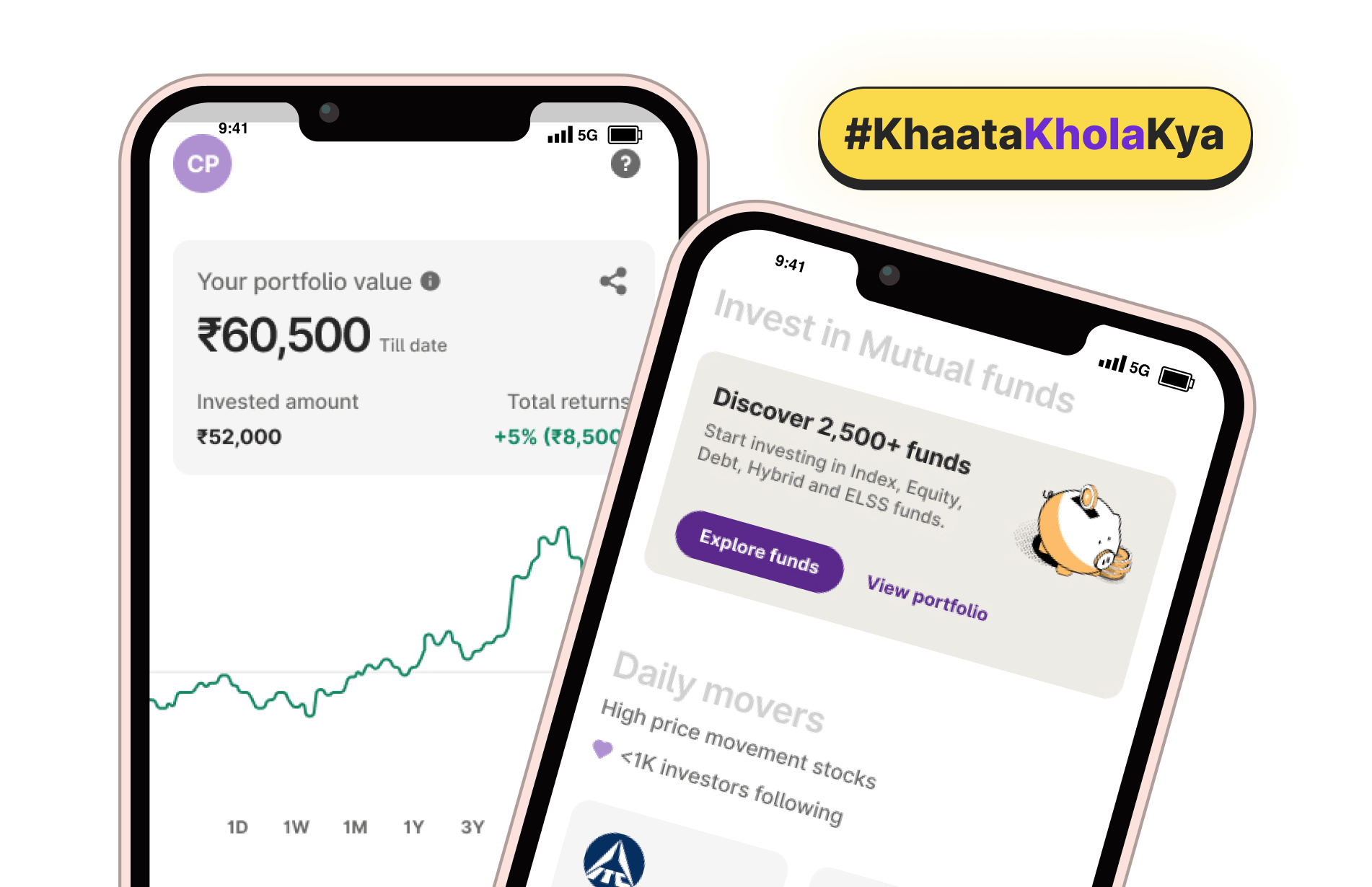

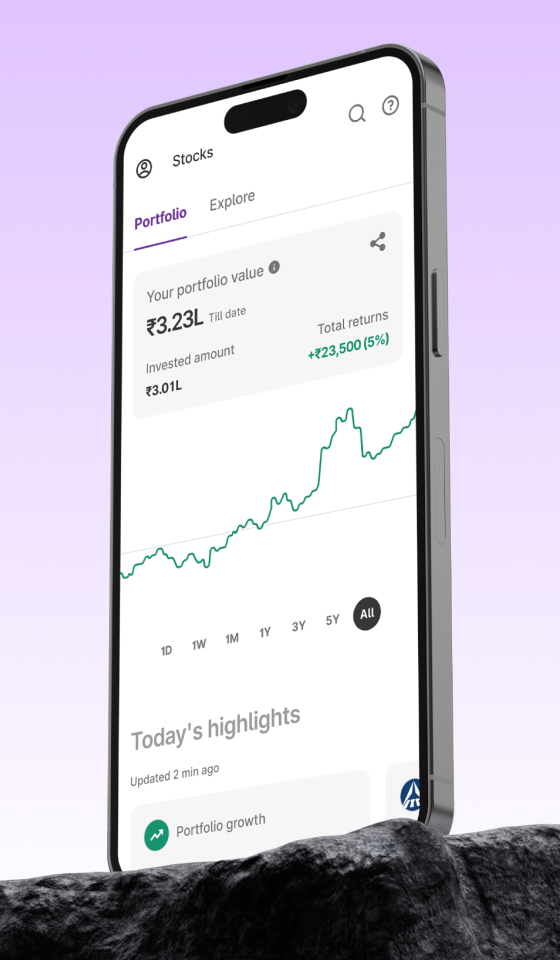

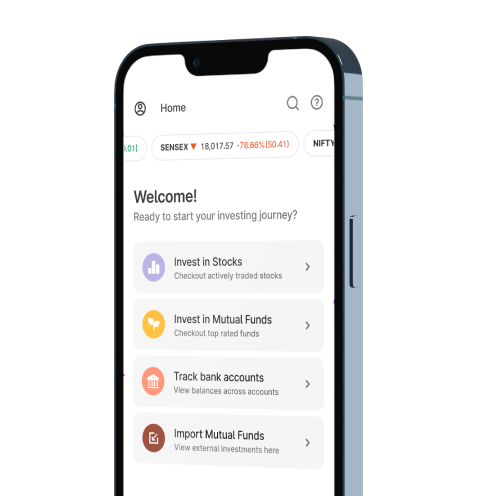

Invest Right, Invest Now in Stocks, Mutual Funds, and IPOs

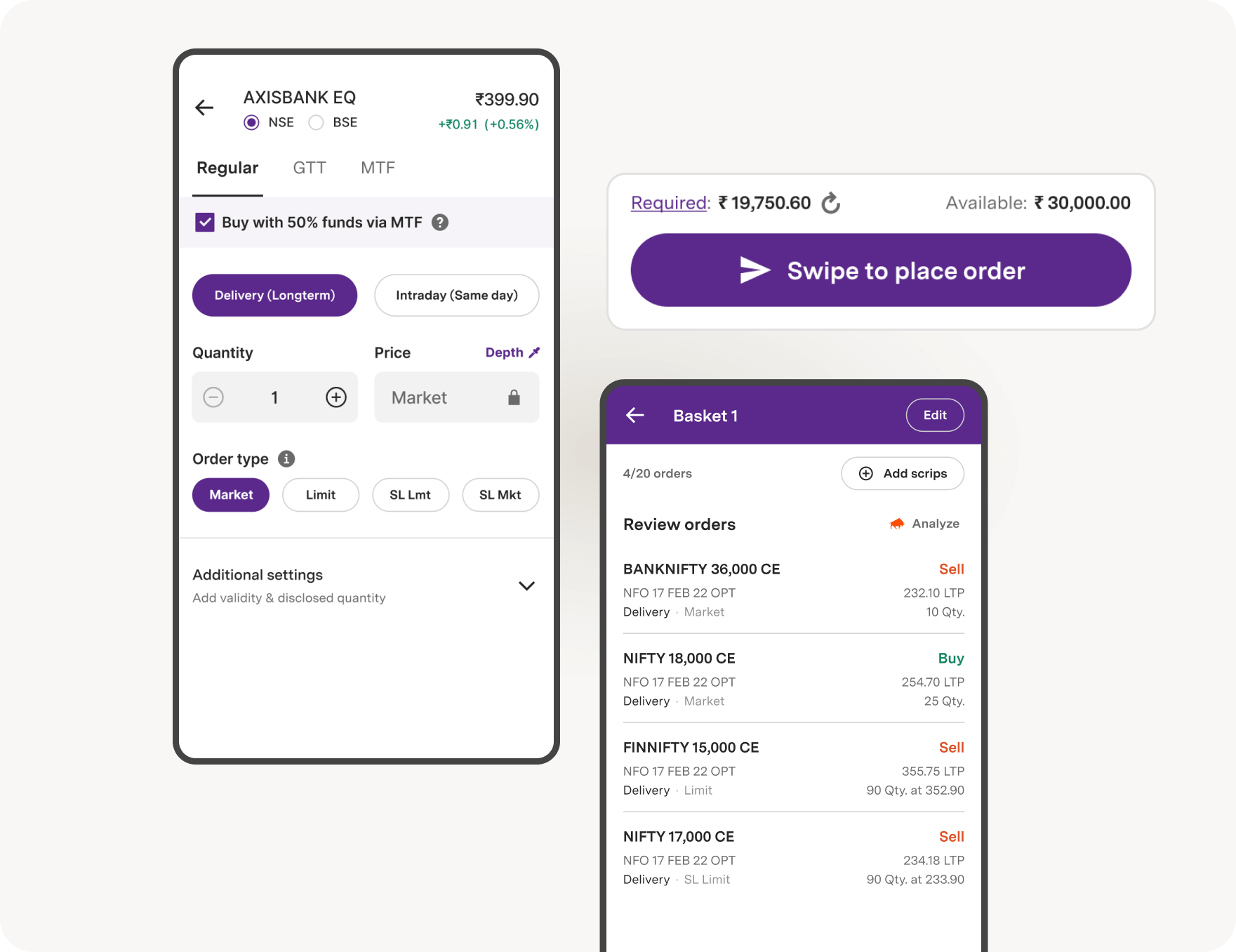

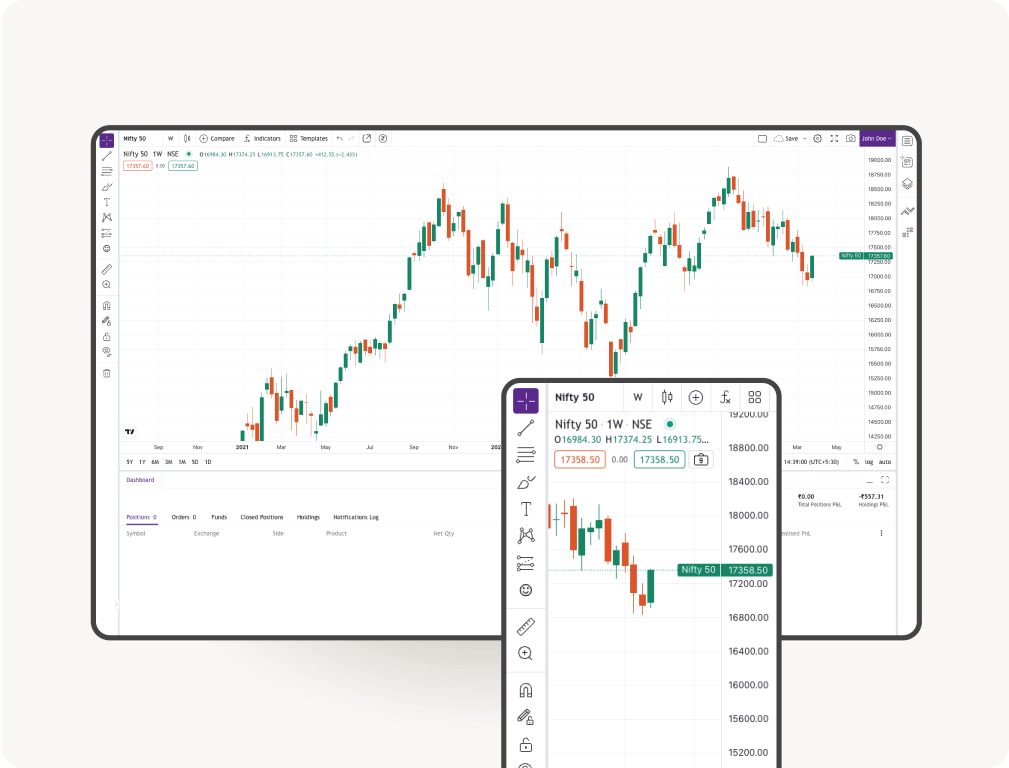

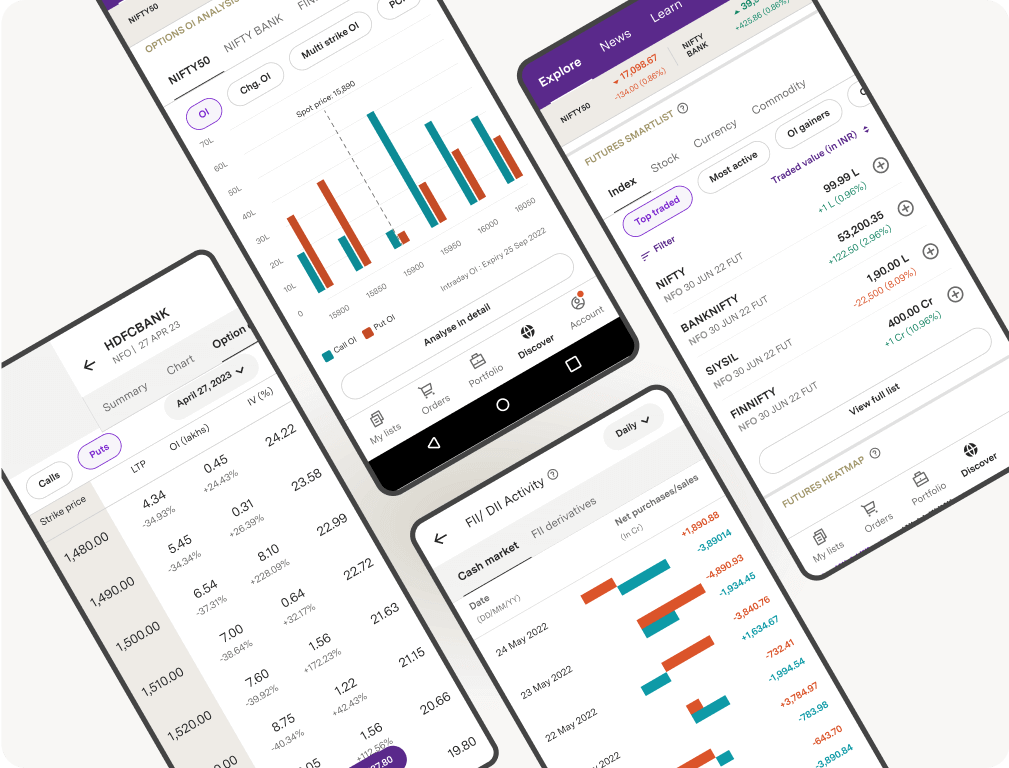

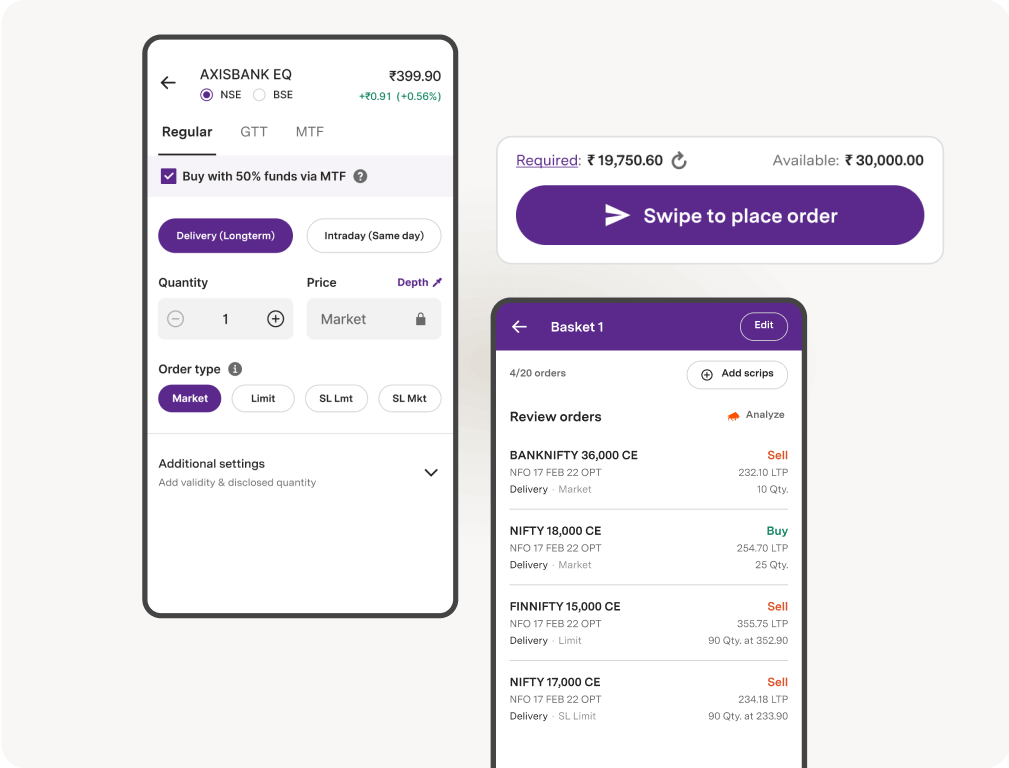

Upstox Pro for Traders

Powerful trading in Equities, Futures, Options, Commodities and Currencies made simple

Learn all about the Stock Market

With our jargon-free and expert-led Courses, Webinars, Events and self-help Videos

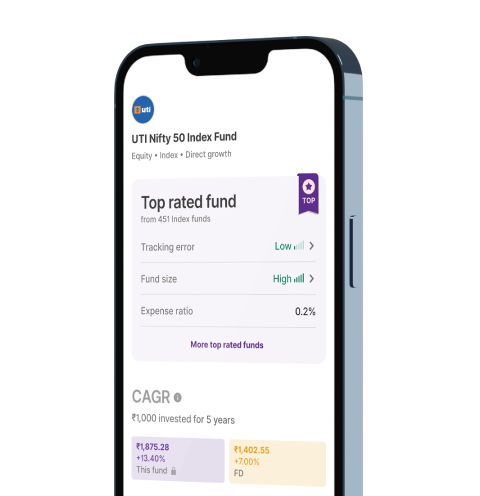

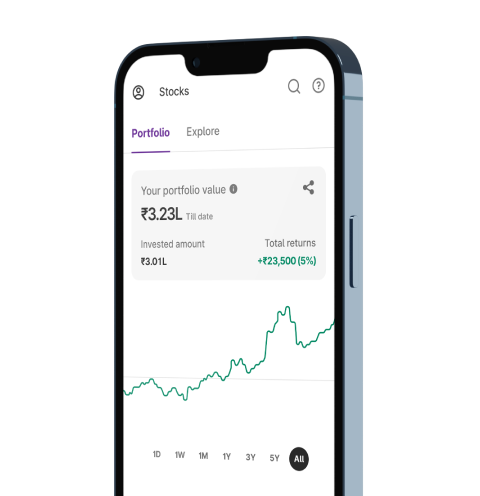

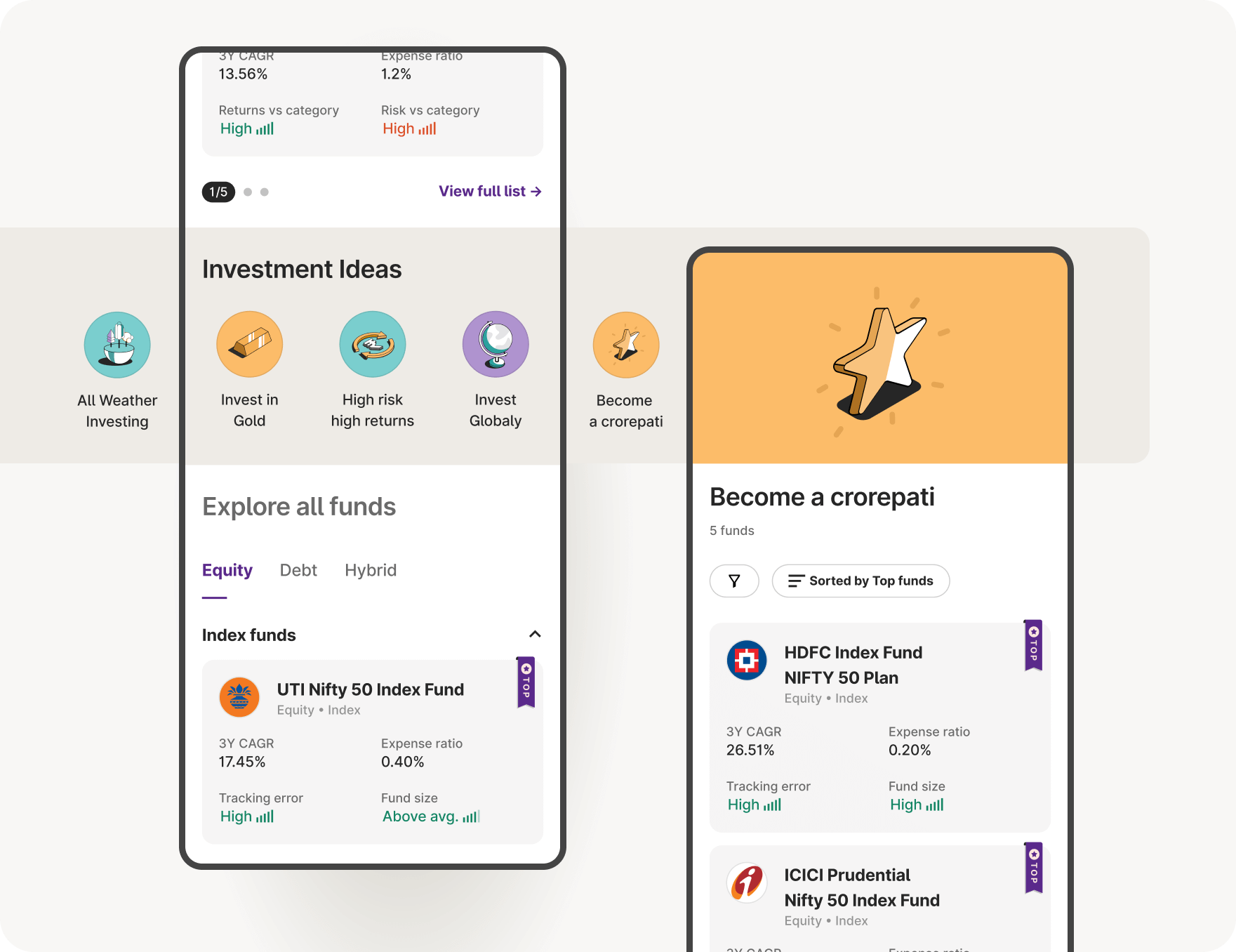

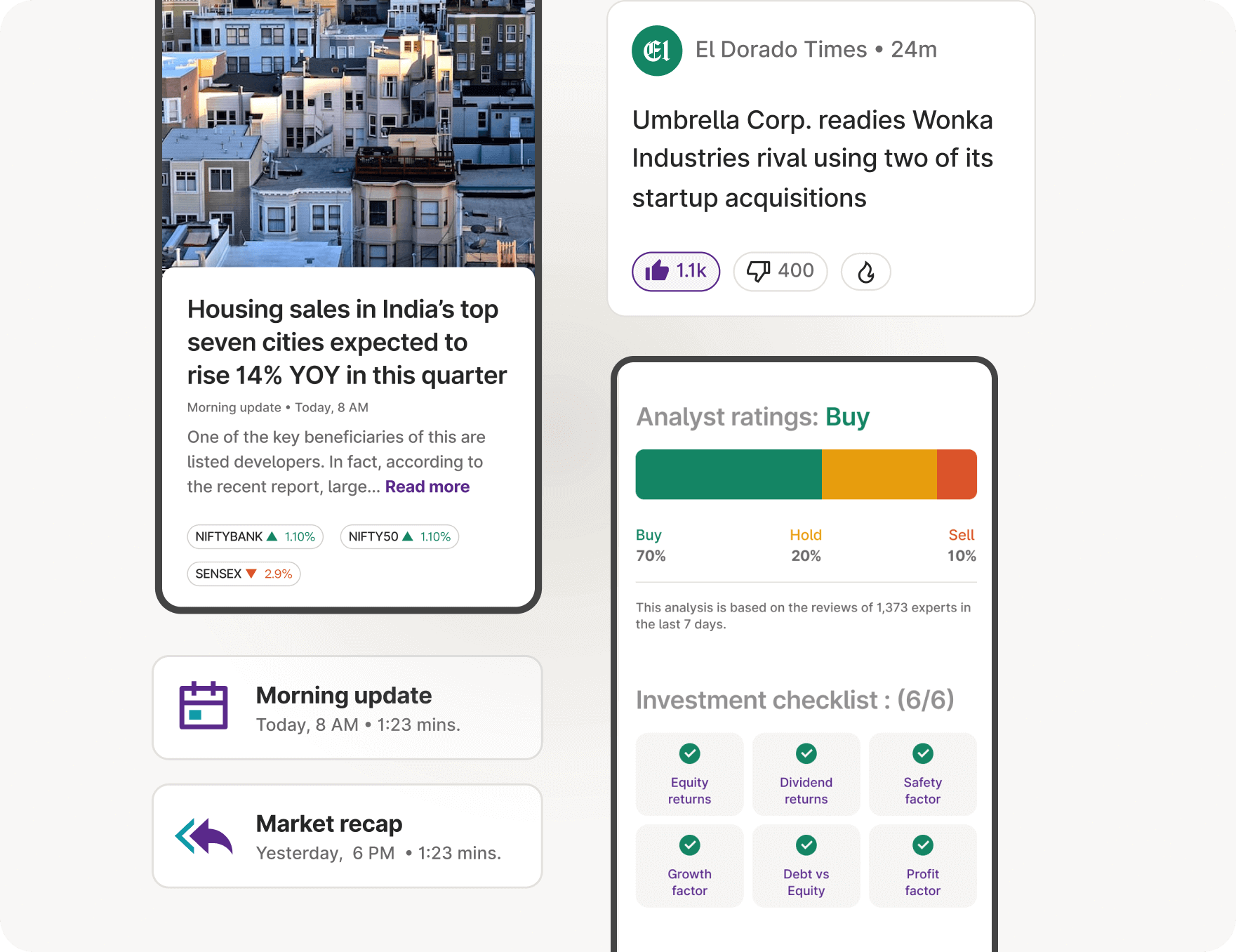

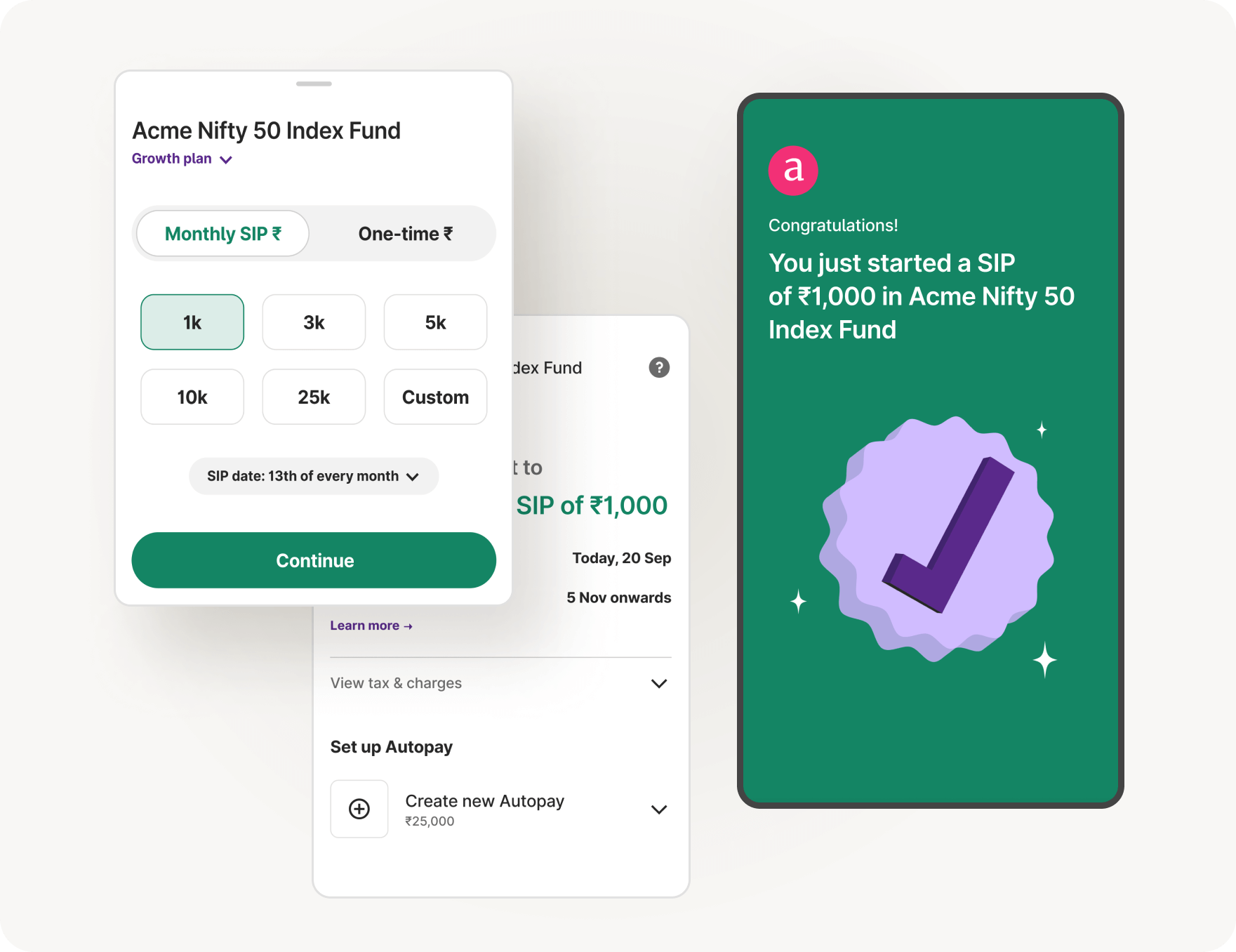

- Top rated funds

- Best for Beginners

- Top 30 actively traded Stocks

- Analyst ratings

- Investment checklist

- Risk & return related info

- Open 24/7

- Pay via UPI

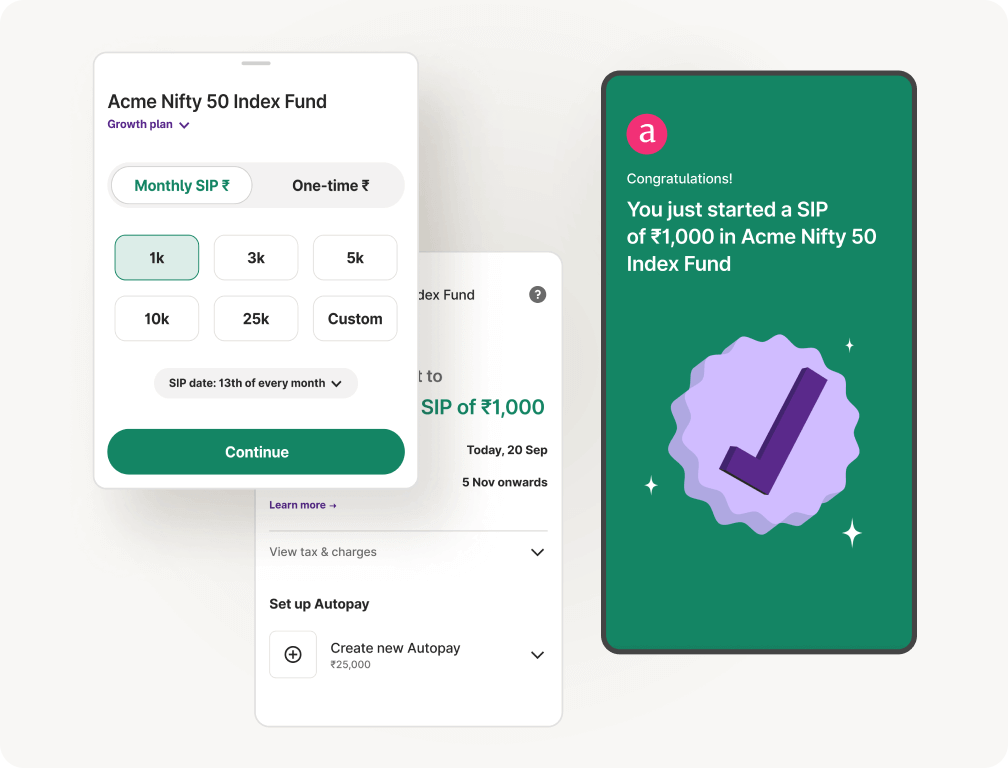

- SIP mode for Stocks & Mutual Funds

Upstox Pro for Traders

Powerful trading in Equities, Futures, Options, Commodities and Currencies made simple

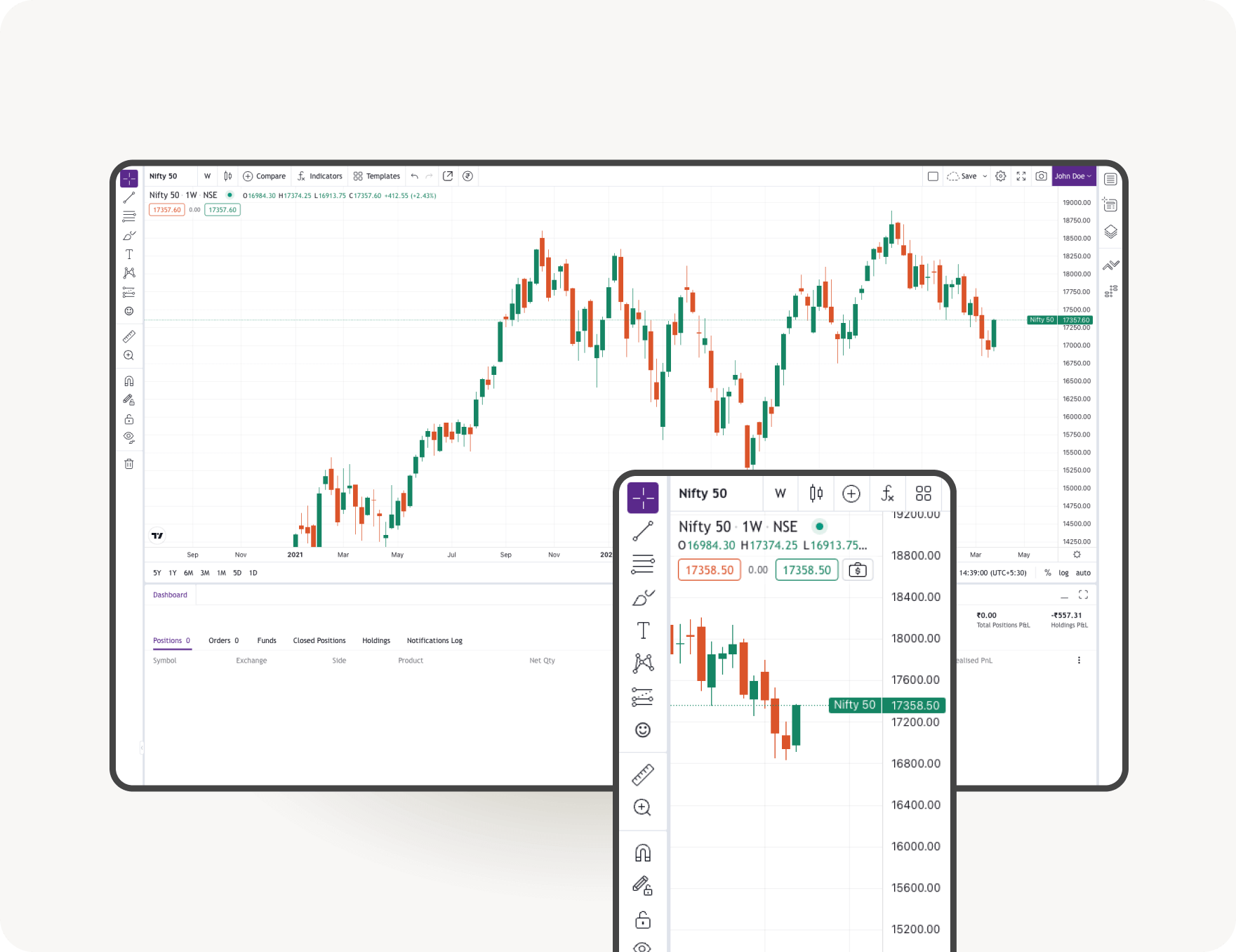

Learn more- TradingView

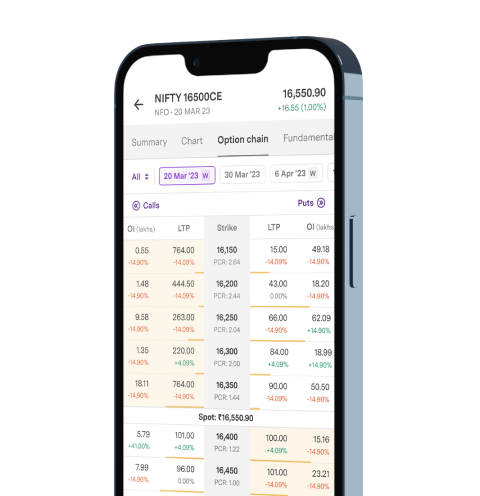

- 8 Charts at once

- 100+ Indicators

- 80+ Drawing tools

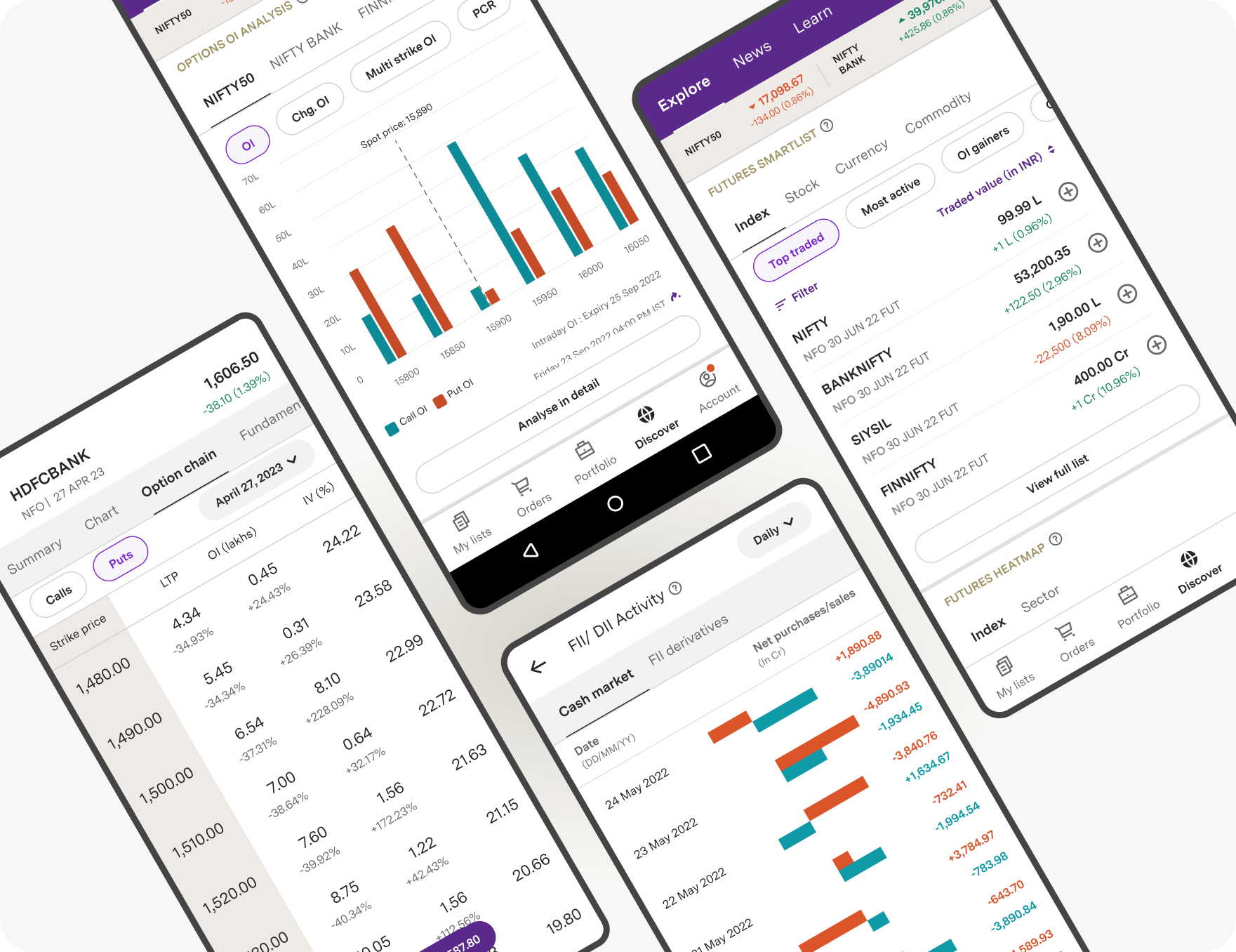

- OI Analysis

- Option Chain with Greeks

- FII & DII Data

- F&O Smartlists

- GTT

- Basket orders, with up to 10 orders

- 2X Margin via Margin Pledge on 450+ Stocks

Learn all about the Stock Market

With our jargon-free and expert-led Courses, Webinars, Events and self-help Videos

#InvestRightInvestNow

Know our storyTransparent pricing. No hidden charges.

View pricing*Zero AMC is applicable for customers onboarded after August 2021

0

Demat + Trading Account Charges

0

Account Maintenance Charges

0

For Mutual Funds and IPOs

20

For Equity, F&O, Commodity and Currency Trades

Calculate Brokerage & Margin easily

- Brokerage Calculator

- Margin Calculator

- Option Strategy Builder

- SIP Calculator

- Mutual Fund Returns Calculator

- SWP Calculator

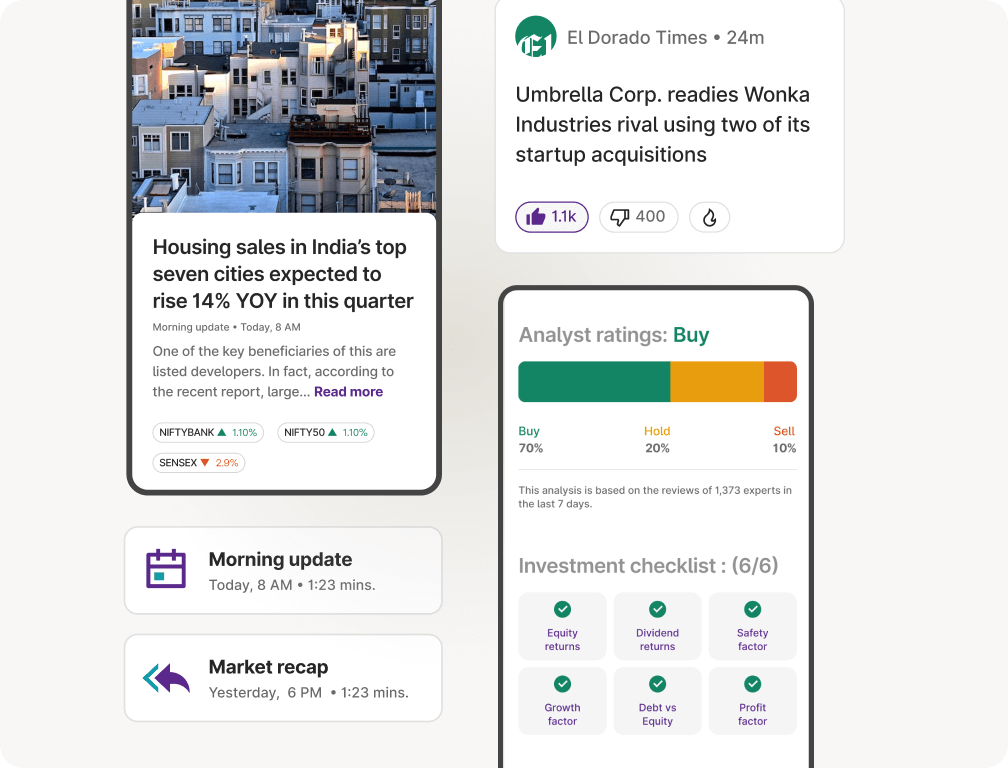

HDFC Bank gets RBI nod to buy stake in IndusInd Bank and Yes Bank, Zydus Life hits 52-week high & more

Pidilite Industries Q3 profit rises, CAMS falls after HDFC Bank sells stake & more

Don’t take our word for it

I like Today's Gainers and Today's Losers in Discover in the Invest section.It helps me plan which Stocks should I invest and which I should not

Baradi Shivakumar

I like the Portfolio News in the Invest section on the Upstox App. It shows News related to the Stocks that are in my Portfolio which helps me in keeping a track of my Stocks status

Naman Nema

I like the option chain section and the way Greeks are displayed as it is very simple to track and make decision to execute orders. It is also easy to "buy" and "sell" positions, UI is very nice

Bhadresh Shah

Where trust matters upstox never breaks.

Bhanu Prasad

The ROS feature is very good and can help the budding option traders to learn with proper discipline and risk management.

Pandi Donald

I like the Chart offered by Upstox, the Candles in the Chart are very clear to view.

Sandeep Shukla

I have been using Upstox for over 5 years now and it has provided me with an awesome experience and excellent customer support. Thanks to Upstox, I have also gained a lot of knowledge about stock market.

Prabhakar Dutta

Download One of India's Best Trading Apps